IRI report indicates small and mid-sized manufacturers losing ground in volume and value to private labels

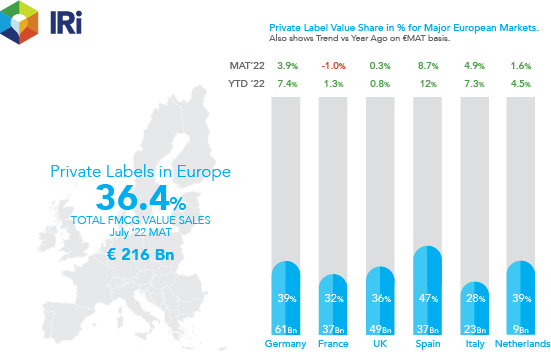

The latest biannual ‘FMCG Demand Signals’ report from IRI has revealed that Private Labels now make up 36% of total FMCG value sales in Europe (€216 billion) – up from 34% as reported by IRI earlier this year. Strong market performance has taken place across all European markets, particularly in Spain where Private Labels now make up 47% of total FMCG value sales; followed by Germany and The Netherlands (both at 39%). The UK and Germany continue to lead Private Labels sales in absolute value.

Forensically unpacking the impact of the pandemic, inflation and the cost of living crisis on over 230 FMCG categories, 2000+ product segments and over a 100 million SKUs across the US and several of the largest European and Asia Pacific markets (France, Italy, Germany, Spain, UK and Netherlands); the report, that covers data from in-store purchases and a survey in 12 global markets.

The report details how fewer promotions by Retailers post-pandemic has made way for a targeted return to lower every day prices across a basket of 150 consumer staples this year; to help mitigate the impact of food-price inflation. Retailers are trying to manage the impact of rising prices by optimising the range, pack sizes and price points but strategies differ by category and value tier – and one of the biggest beneficiaries have been Private Labels.

“Private Labels have traditionally offered lower prices to shoppers,” commented Ananda Roy, Global SVP, Strategic Growth Insights, IRI, “but these are not sustainable and inflationary price rises have been greater than on well-recognised brand names. Yet this has not dampened demand especially in the Chilled and Fresh, Ambient and Frozen segments in food categories, and Household and Personal Care in non-food categories.”

“Our research has shown this is because around 60% of consumers believe Private Labels are as good at National Brands on Quality, Innovativeness, Sustainability, Trust and Delivering on claims, with 25% saying some Private Labels are ‘even better’ than National Brands. This is a significant shift from previous periods.

“It’s fair to say that Private Labels are poised to be the ‘third competitor’ to National Brands in several FMCG categories, having transformed to strategy-led, data-driven & differentiated substitutes. Their ability to grow value, volume and attract new consumers is a growing risk to smaller and mid-sized manufacturers – the ‘Squeezed Middle’ – who could begin to struggle to match Private Labels competitively as economic conditions worsen. IRI anticipates that a price war is increasingly likely in early 2023 and thereafter as the outlook for FMCG demand darkens.”

Another recent trend is among UK Retailers who have created new products with artisanal food brands from small manufacturers or restaurant chains to add brand recognition & quality perception in their Private Label portfolio in order to command a premium margin.

Post pandemic to today

Throughout the pandemic, national brands outperformed Private Labels – with consumers feeling comforted by buying brands they knew, trusted and could easily find in-store or online in challenging times. In the current inflationary environment, Private Labels are returning to pre-pandemic levels as consumers question their loyalty to National Brands, and Retailers expand the range of high quality, innovative and well-priced options. Discounters have expanded their portfolio of small-format stores in town centres and residential neighbourhoods making these products available to a wider group of consumers who may not have been willing to travel to out-of-town stores previously. This has led to value sales growing +5.4% in the year-to-date 2022 (+3.0% MAT 2022). Notably only Italy is showing robust growth in both Private Labels and National Brands.

Key drivers

The growth in 2022 to date is being primarily driven by Food categories (+5.3%), taking its contribution to €191Bn, with Chilled & Fresh, Frozen and Beverage categories growing. Notably though is Alcohol which has seen a decline of 5% or £3.4Bn in value sales to July 22 in comparison to a year ago and 6.7% in the year-to-date 2022.

Non-edible Private Labels are growing at pace in two of the biggest Private Label markets – Germany & Spain – and across Europe at three times of the total Private Labels market in the last four weeks alone delivering €25 billion.