The Great Reset – IGD Maps Out Four Post-lockdown Scanarios For Retail and Foodservice

COVID-19 has caused a monumental shift in consumers’ food and drink habits. The boundaries between eating at home and out-of-home, once blurred, have now broken down, resulting in unprecedented changes to supply and demand of food and drink in the UK.

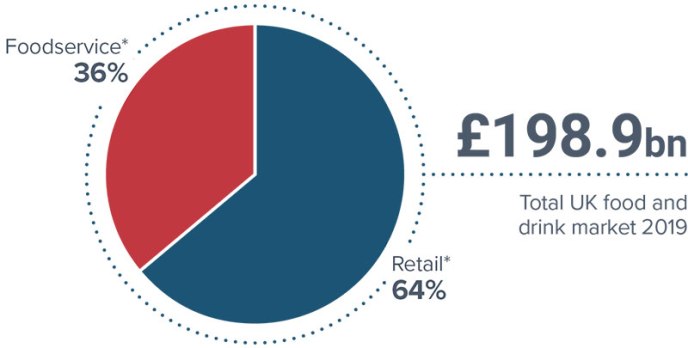

In 2019, the split of consumer spend on food and drink was one-third (36%) in foodservice and two-thirds (64%) in retail. In 2020, COVID-19, the resulting lockdown measures and closure of all non-essential shops, pubs, restaurants and cafes, will have a dramatic impact on the balance of consumer spend in retail and foodservice.

Eating In Vs Dining Out, new research from IGD produced in collaboration with leading foodservice consultant Peter Backman, explores the impact of COVID-19, outlining four potential scenarios to help food retail and foodservice companies plan for the future. Each scenario addresses the possible path of the virus and performance of the economy; from a relatively manageable virus to multiple outbreaks, and an economic performance that quickly recovers to a hard-hit economy, slow to rebuild.

The four hypothetical scenarios are:

- The Great Reset: This most positive scenario sees food and drink consumption largely shift to home. Retail sales remain high but flatten as lockdown restrictions gradually lift and people start to eat out again. Safety and hygiene in out-of-home settings have higher value for consumers and become a key factor as they choose where to eat and drink. Some changes in consumer behaviour become the norm, fuelling further development of digital channels. Eating out returns to levels experienced in 2019 in two years’ time.

- Decade of Drift: In this scenario, the virus is manageable, but the economy takes longer to recover and the financial impact on households and businesses is severe. Companies accelerate cost-cutting and efficiency programmes to demonstrate value to consumers, resulting in lower levels of new product development. Demand for eating out among consumers is high, but many are unable to afford it.

- Technical Isolation: The path of the virus sees businesses and consumers turn to technology and digital services, which reshapes the retail offer; online is seen as the safest way to shop. Businesses divert investment from stores and shopping is a functional activity. Eating out is also functional and severely constrained. Stores and foodservice sites that cannot be repurposed to increase online capability will close.

- Globalisation reversed: This is the most severe scenario, combining bad outcomes for both the virus and the economy. Globalisation regresses, putting pressure on supply chains and businesses to find operational efficiency. Supply chains need extensive rebuilding; ranges change, with some products becoming seasonal or disappearing completely. For commercial foodservice, deliveries and takeaway services are almost the only option due to increased costs and complexity.

Rhian Thomas, Head of Shopper Insight at IGD, says: “COVID-19 has resulted in the boundaries between in-home and out-of-home consumption breaking down further and faster than any of us could have imagined. The future is unpredictable; we don’t know what path the virus will take or how lockdown measures will affect the performance of markets in the medium to longer term.

Rhian Thomas, Head of Shopper Insight at IGD.

“In this highly uncertain environment, it is crucial that retailers and suppliers are able to respond successfully and quickly to events as they unfold. Considering which changes in shopper behaviour will become permanent will help identify the solutions that you want your business to nurture.

“Foodservice companies must balance customer focus with practical, operational issues and work collaboratively with partners to achieve this. Much thought must be given to the best time to reopen and foodservice companies must be prepared to rewrite their business plans with a start-up mentality.”

Peter Backman, foodservice consultant and co-author of the report, comments: “COVID-19 has been, and will continue to be, a great accelerator for the shifts between in and out of home consumption that have been emerging over the past 15 years. Current consumer behaviour is a catalyst for change, which is happening far faster than anything I predicted, just six months ago. As we move forward, every part of the supply chain will have to be able to adapt rapidly to this changing landscape.

“The hospitality industry has taken an unimaginable hit, but many operators have used it as an opportunity to pivot their businesses and redefine both their offer and the way it’s delivered. The entrepreneurial spirit and dedication to save a much-loved industry has been refreshing for all to see.

“Consumer demand will drive and shape the eating in and dining out markets more than ever before, so suppliers, foodservice operators and retailers will need to react, adjust and innovate to allow for evolving scenarios. The food industry has always been fast-paced; it’s about to get faster.”

Eating In Vs Dining Out is available to subscribers on IGD Retail Analysis, further insight can also be found here.